Call Us For Easy

Confidential Assistance

503-506-0101

It only takes 5 minutes to get started

Using Private Health Insurance for Addiction Treatment in Oregon

Posted on: June 18th, 2026 by writer

Table of Contents

- The Hidden Crisis: Why So Many Oregonians Don’t Get the Help They Need

- Your Legal Right to Addiction Coverage: How MHPAEA and the ACA Changed Everything

- Insurance 101: Understanding Deductibles, Co-Insurance, and Out-of-Pocket Maximums

- No Surprises: How We Verify Your Insurance Benefits Before You Admit

- Case Study: How John Used His PPO Plan to Get Treatment (and Paid Less Than He Expected)

- What’s More Expensive: Treatment or Continued Addiction?

- Final Thoughts

The decision to seek help for addiction is one of the most courageous steps anyone can take. Yet for many Oregonians, a painful question often delays or even prevents that critical first step: “How will I afford residential treatment?”

If you’re among the thousands of Oregon residents struggling with substance use, you’re not alone in this financial concern. The fear of medical bankruptcy, overwhelming bills, and financial uncertainty keeps far too many people from accessing life-saving care. But here’s the truth that might surprise you: thanks to federal law, your private health insurance is legally required to cover addiction treatment on the same terms as it covers conditions like diabetes or heart disease.

The numbers tell a sobering story. Approximately 18.2% of Oregonians aged 12 or older meet the criteria for a substance use disorder. Despite this staggering need, cost and lack of insurance coverage remain the most frequently cited barriers preventing people from getting help. But what many don’t realize is that the landscape of addiction treatment coverage has fundamentally changed over the past decade.

This guide will walk you through exactly how your private health insurance works for residential addiction treatment in Oregon. You’ll discover what you’ll actually pay out-of-pocket, how facilities like Pacific Ridge make the admissions process transparent and financially manageable, and why the perceived cost of treatment is often dramatically different from the reality.

By understanding your insurance benefits upfront, you can eliminate the financial anxiety that may be holding you back and focus on what truly matters—your recovery.

The Hidden Crisis: Why So Many Oregonians Don’t Get the Help They Need

Oregon faces a behavioral health paradox that affects thousands of families. Our state consistently ranks among the highest in the nation for rates of substance use disorders, yet simultaneously ranks among the lowest for treatment access. This “treatment gap”—the chasm between those who need help and those who receive it—represents one of our most pressing public health challenges.

The perception that residential addiction treatment is financially out of reach creates a devastating barrier. Many Oregonians assume that a 30-day residential program will cost tens of thousands of dollars out-of-pocket, making treatment seem impossible for working families. This assumption keeps people trapped in the cycle of addiction, often for years, when help is actually far more accessible than they realize.

According to national surveys, among adults with substance use disorders who recognized they needed treatment but didn’t receive it, cost and lack of insurance coverage topped the list of reasons. This financial anxiety isn’t just preventing treatment—it’s perpetuating a public health crisis.

What makes this particularly tragic is that most private insurance plans are legally mandated to cover addiction treatment comprehensively. The gap isn’t in coverage—it’s in awareness and understanding.

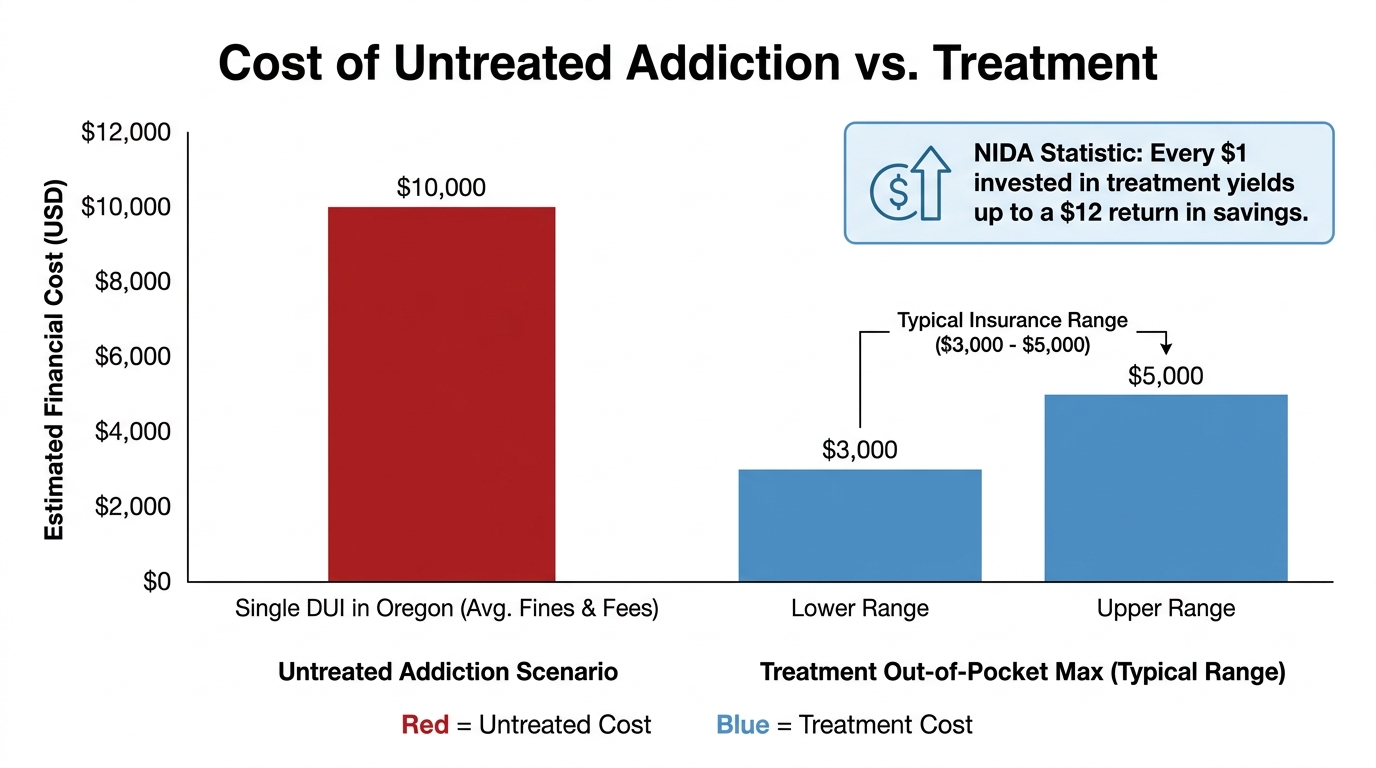

The emotional and financial toll of delaying treatment extends far beyond the individual suffering from addiction. Untreated substance use disorders lead to emergency room visits, legal complications, lost employment, fractured relationships, and chronic health conditions. A single DUI in Oregon can cost upwards of $10,000 when you factor in fines, legal fees, mandatory education programs, and increased insurance premiums. The ongoing costs of active addiction—lost wages, medical crises, legal troubles—quickly dwarf the out-of-pocket costs of getting comprehensive treatment.

The solution begins with understanding a fundamental truth: your existing private health insurance is designed to make residential treatment affordable. Federal law protects this right, and facilities throughout Oregon work within these insurance frameworks to provide transparent, predictable costs that most working families can manage.

Your Legal Right to Addiction Coverage: How MHPAEA and the ACA Changed Everything

Understanding how we arrived at today’s insurance landscape is crucial to recognizing just how protected you are when seeking addiction treatment.

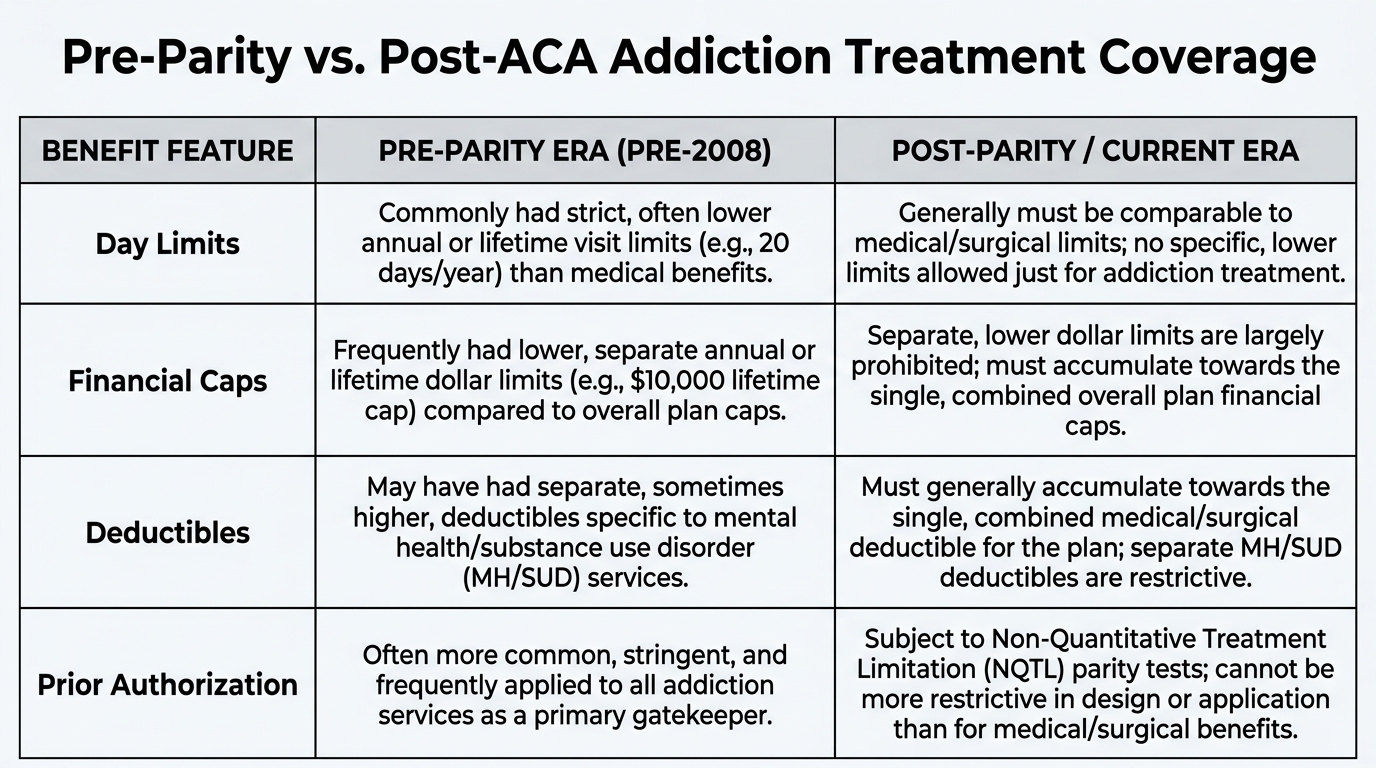

Before 2008, the insurance industry routinely discriminated against behavioral health conditions. Insurers could—and regularly did—impose strict annual limits on residential addiction treatment, often capping coverage at just 14 days per year regardless of medical necessity. They maintained separate, higher deductibles specifically for mental health and substance use services. Lifetime dollar caps meant that even if you received some coverage, you might exhaust your benefits entirely, leaving you vulnerable if you ever needed help again.

This discriminatory landscape changed dramatically with two landmark pieces of federal legislation.

The Mental Health Parity and Addiction Equity Act (MHPAEA) of 2008 fundamentally transformed how insurers must treat behavioral health coverage. This federal law requires that health insurance plans offering mental health and substance use disorder benefits provide those benefits on equal terms with medical and surgical care. Insurers cannot impose tighter financial requirements—like higher copayments or separate deductibles—on addiction treatment than they do for treating a broken bone or managing diabetes. They cannot set stricter treatment limitations either, such as arbitrary day limits on residential care.

Building on this foundation, the Affordable Care Act (ACA) of 2010 designated mental health and substance use disorder services as one of ten “Essential Health Benefits.” This means that all non-grandfathered individual and small group commercial plans in Oregon must include addiction treatment coverage. It’s not optional or supplemental—it’s a core, mandatory component of comprehensive health insurance.

What does this mean for you in practical terms? Your insurance plan cannot arbitrarily limit how many days of residential treatment you can receive in a year. Coverage is determined by medical necessity—what clinicians determine you need to achieve stable recovery—not by outdated insurance policies. Your plan cannot impose lifetime dollar limits on addiction care. And the financial requirements you face for addiction treatment must align with what you’d face for any other medical condition.

These protections represent a seismic shift in how addiction treatment is covered, understood, and accessed. They transformed addiction care from a marginalized, poorly covered service into a protected essential health benefit with the same standing as emergency care or prescription medications.

Insurance 101: Understanding Deductibles, Co-Insurance, and Out-of-Pocket Maximums

Let’s demystify the insurance terminology that determines what you’ll actually pay for residential addiction treatment. Understanding these four key concepts will transform abstract financial anxiety into concrete, manageable numbers.

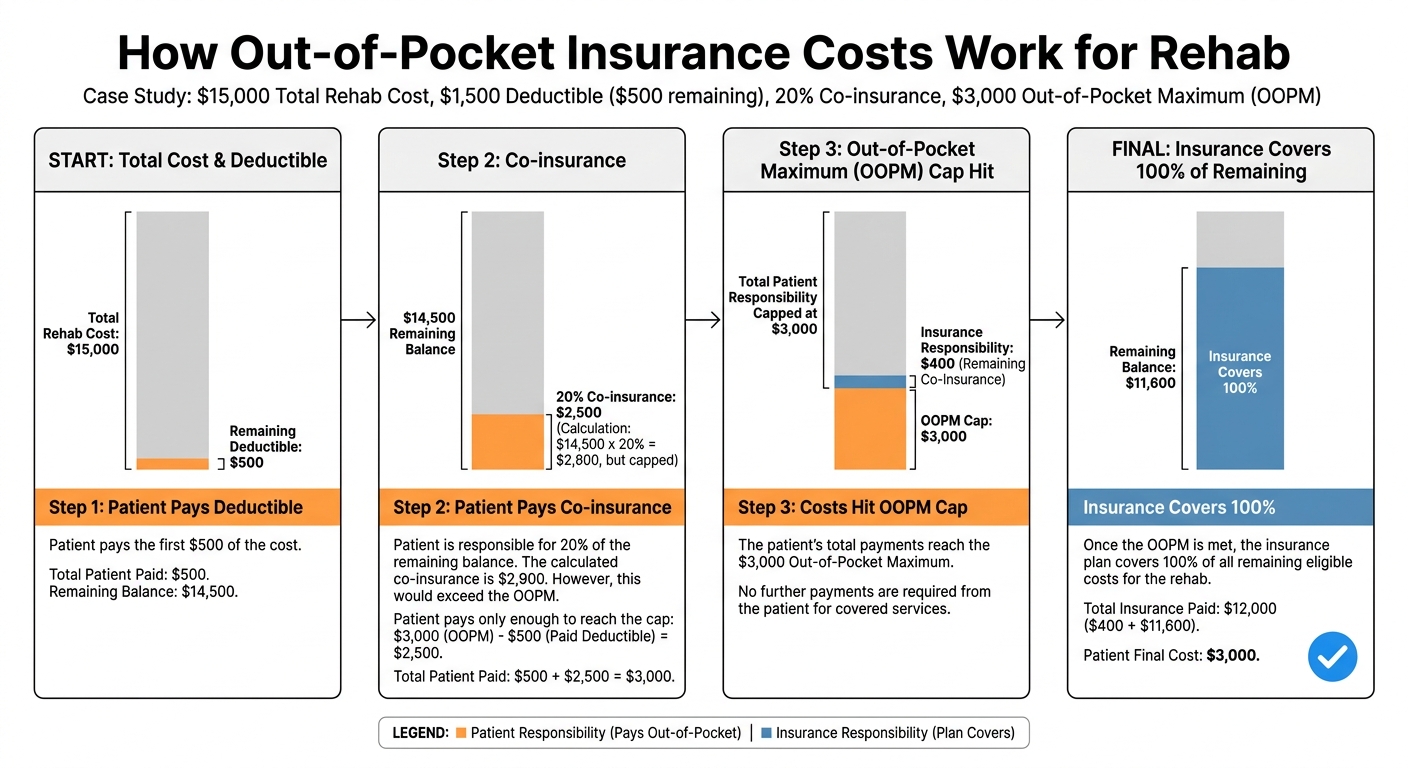

Your Deductible is the amount you pay for healthcare services before your insurance coverage kicks in. Think of it as the threshold you must cross before your insurance company begins sharing costs. If your deductible is $2,000 and you haven’t had any medical expenses yet this year, you’ll pay the first $2,000 of your residential treatment costs before insurance contributes.

Co-Insurance is the percentage split between you and your insurance company after you’ve met your deductible. The most common arrangement is an 80/20 split, where your insurance covers 80% of approved costs and you’re responsible for the remaining 20%. For example, if your treatment costs $15,000 and you’ve already met your deductible, you would pay 20% of that amount ($3,000) while insurance covers the other $12,000.

But here’s the most important number—the one that provides the greatest financial reassurance:

Your Out-of-Pocket Maximum (OOPM) is the absolute ceiling on what you’ll pay for covered healthcare services in a calendar year. Once you’ve paid this amount through deductibles, co-insurance, and copayments, your insurance pays 100% of all covered, medically necessary services for the remainder of the year. This is your financial safety net.

For most Oregon residents with employer-sponsored or marketplace plans, out-of-pocket maximums typically range from $3,000 to $9,000 for individual coverage. While these numbers might initially seem significant, they represent your maximum possible financial responsibility—no matter how much your treatment actually costs.

This means that even if a 30-day residential addiction program has a total cost of $20,000, you will never pay more than your out-of-pocket maximum. And if you’ve already had medical expenses earlier in the year, you may have already paid toward that maximum, further reducing what you’ll owe for treatment.

In-Network vs. Out-of-Network considerations also play a crucial role. In-network facilities have negotiated rates with your insurance company, which typically results in significantly lower out-of-pocket costs. Pacific Ridge works with major Oregon insurance carriers including Moda Health, PacificSource, Providence Health Plan, Regence BlueCross BlueShield, and Kaiser Permanente, maximizing the likelihood that you’ll receive in-network benefits.

Let’s look at a concrete example to see how these pieces fit together:

Sarah’s Insurance Scenario:

Sarah has private insurance with a $1,500 deductible, 20% co-insurance, and a $4,000 out-of-pocket maximum. Earlier this year, she had a minor surgery that cost $1,000, which she paid entirely since she hadn’t yet met her deductible.

When Sarah seeks residential addiction treatment:

- She owes the remaining $500 to meet her deductible

- After that, she pays 20% co-insurance on subsequent costs

- Her total financial responsibility for the entire year is capped at the remaining $3,000 to reach her out-of-pocket maximum

Instead of paying $15,000-$20,000 for a comprehensive 30-day residential program, Sarah’s maximum cost is $3,000—and possibly less if her treatment costs don’t push her all the way to her out-of-pocket maximum.

This is the financial reality that insurance provides. It transforms treatment from “impossible” to manageable for most Oregon families.

No Surprises: How We Verify Your Insurance Benefits Before You Admit

One of the most significant sources of anxiety around addiction treatment is financial uncertainty. How much will this actually cost me? What if I can’t afford it once I’m already admitted? What if there are hidden fees or surprise bills months later?

The Verification of Benefits (VOB) process eliminates this uncertainty entirely, providing complete financial transparency before you make any commitment.

When you contact Pacific Ridge or any reputable treatment facility, the admissions team initiates a comprehensive benefits verification with your insurance company. This isn’t a superficial check—it’s a detailed investigation into your specific coverage that answers every critical financial question.

During the VOB process, admissions specialists contact your insurance carrier directly to confirm:

- Your current deductible status, including how much you’ve already paid toward your deductible this calendar year

- Your co-insurance percentage for behavioral health and substance use services

- Your out-of-pocket maximum and how much you’ve already contributed toward it

- Whether prior authorization is required for residential treatment and, if so, initiating that authorization process

- The specific coverage details for the level of care being recommended

- Any exclusions or limitations that might apply to your particular plan

This process typically takes 24-48 hours and results in a written cost estimate that clearly outlines your financial responsibility. You’ll know your exact costs before you admit—no guessing, no surprises, no hidden fees discovered months later.

The transparency this provides is transformative. Instead of the paralyzing question “Can I afford this?”, you receive clear, concrete answers: “Based on your current insurance benefits, your estimated out-of-pocket cost for a 30-day residential program is $X,XXX.” This transforms an abstract fear into a manageable financial decision.

For many prospective patients, this moment of clarity—understanding their actual financial obligation—is what finally allows them to move forward with treatment. They’ve often delayed seeking help for months or even years due to cost uncertainty. The VOB process removes that final barrier.

Pacific Ridge’s admissions specialists also handle all communication with your insurance company regarding prior authorization requirements. Many insurance plans require pre-approval for residential treatment, and navigating this process can be complex. By managing this administrative burden, treatment facilities ensure that financial and bureaucratic obstacles don’t delay your access to care.

This commitment to transparency extends throughout your treatment. You’ll receive regular updates about your insurance coverage, any changes in your financial responsibility, and clear, itemized billing that shows exactly what your insurance covered and what you owe.

Case Study: How John Used His PPO Plan to Get Treatment (and Paid Less Than He Expected)

Understanding insurance benefits in abstract terms is helpful, but seeing how they work in a real-world scenario often provides the clarity and reassurance people need to move forward. John’s story illustrates how private insurance transforms the affordability of residential addiction treatment.

The Background:

John, a 35-year-old Portland resident, had been struggling with severe alcohol use disorder for years. He recognized he needed help and had researched residential treatment programs, but consistently put off making the call. His assumption was straightforward: a 30-day residential program would cost somewhere between $15,000 and $20,000 out-of-pocket, which felt completely unaffordable on his salary.

John had employer-sponsored health insurance through Regence BlueCross BlueShield—a comprehensive PPO plan—but he’d never explored how it might cover addiction treatment. He assumed that behavioral health coverage was minimal or came with massive out-of-pocket costs. This assumption kept him from seeking help for two additional years, during which his drinking worsened, his relationships deteriorated, and he received a DUI that cost him over $8,000 in legal fees and fines.

The Intervention:

When John finally reached out to a treatment facility, the admissions team immediately initiated a Verification of Benefits. Within 24 hours, they provided him with a complete financial breakdown.

John’s insurance plan included:

- A $1,500 annual deductible

- 20% co-insurance for behavioral health services

- A $4,000 out-of-pocket maximum

The admissions team also discovered that John had already paid $1,000 toward his deductible earlier that year for general medical expenses (an urgent care visit and some prescription medications). This meant he only had $500 remaining to meet his deductible.

The Financial Reality:

Based on this benefits verification, John’s financial responsibility broke down as follows:

- He would pay the remaining $500 to meet his annual deductible

- After meeting his deductible, he would be responsible for 20% co-insurance on the cost of treatment

- However, his total costs for the entire year—including the $1,000 already paid and any treatment costs—could not exceed his $4,000 out-of-pocket maximum

This meant John’s absolute maximum financial liability for comprehensive residential addiction treatment was $3,000 (the remaining amount to reach his out-of-pocket maximum). In reality, depending on the final costs and how insurance processed claims, he might pay even less.

The Outcome:

When John realized that instead of paying $15,000-$20,000, his maximum cost would be $3,000—less than half of what he’d already spent on his DUI—the financial barrier that had kept him from treatment for years dissolved immediately.

He admitted himself to treatment the following week and completed a 30-day residential program. His final out-of-pocket cost was $2,850. For the remainder of that calendar year, he attended outpatient therapy and counseling sessions, all of which were covered at 100% because he’d reached his out-of-pocket maximum.

John has been in recovery for over two years now. When reflecting on his journey, he often mentions that the VOB process—understanding his actual financial responsibility—was the turning point that finally allowed him to seek help.

This case illustrates a pattern we see repeatedly: the perceived cost of addiction treatment is dramatically higher than the reality when you understand how private insurance works. The assumptions and fear around cost keep people suffering unnecessarily, when transparent benefits verification could provide immediate clarity and relief.

What’s More Expensive: Treatment or Continued Addiction?

When discussing the cost of residential addiction treatment, it’s essential to consider the alternative. What is the financial impact of not seeking treatment?

Substance abuse carries an enormous economic burden, both nationally and individually. Across the United States, substance use disorders cost society over $600 billion annually in crime-related expenses, lost workplace productivity, and healthcare costs. While these national figures are staggering, the personal financial toll of untreated addiction affects individuals and families directly.

The Hidden Costs of Active Addiction:

Emergency room visits for overdoses, injuries, or complications from substance use can cost thousands of dollars per visit, with minimal insurance coverage for non-admitted ER care. Legal consequences create devastating financial burdens—a single DUI in Oregon typically exceeds $10,000 when you account for fines, court fees, mandatory education programs, attorney costs, and dramatically increased auto insurance premiums that can last for years.

Lost employment or reduced earning potential represents perhaps the most significant long-term financial impact. Addiction frequently leads to job loss, reduced hours, missed promotions, or the inability to pursue career advancement. Over time, this lost income far exceeds any out-of-pocket costs for treatment.

The physical health consequences of long-term substance use also carry substantial costs. Liver disease, cardiovascular problems, infectious diseases, and chronic conditions all require expensive ongoing medical care, often without the same insurance protections that cover addiction treatment itself.

The Return on Investment of Treatment:

Research from the National Institute on Drug Abuse provides compelling evidence that addiction treatment isn’t just a healthcare expense—it’s a high-return investment. Studies demonstrate that every dollar invested in addiction treatment programs yields between $4 and $7 in reduced drug-related crime, criminal justice costs, and theft. When you factor in healthcare savings—reduced emergency room visits, fewer hospitalizations, better management of co-occurring conditions—the total savings can exceed costs by a ratio of 12 to 1.

For individuals and families, the math is even more straightforward. Consider a typical scenario:

| Cost Category | One Year of Untreated Addiction | Treatment Investment |

|---|---|---|

| Emergency Room Visits | $6,000 – $9,000 | — |

| Legal Fees (DUI/Possession) | $8,000 – $15,000 | — |

| Lost Wages | $5,000 – $15,000 | — |

| Relationship Counseling/Divorce | $3,000 – $10,000 | — |

| Health Complications | $2,000 – $5,000 | — |

| Out-of-Pocket Maximum for Residential Treatment | — | $3,000 – $5,000 |

| Outpatient Follow-up Care | — | $0 – $500 |

| TOTAL | $24,000 – $54,000 | $3,000 – $5,500 |

The financial case for treatment becomes overwhelming when you view it through this lens. Even in purely economic terms—setting aside the immeasurable value of restored health, rebuilt relationships, and reclaimed life—treatment represents extraordinary value.

Moreover, once you’ve reached your out-of-pocket maximum through residential treatment, all subsequent covered behavioral health services for that calendar year are provided at no additional cost. This means ongoing therapy, counseling, medication-assisted treatment, and other support services become fully covered, creating a comprehensive pathway to sustained recovery at no additional expense.

The question isn’t “Can I afford treatment?” The real question is “Can I afford not to get treatment?”

Final Thoughts

The path to recovery from addiction shouldn’t be blocked by financial fear and uncertainty. Thanks to federal protections established through the Mental Health Parity and Addiction Equity Act and the Affordable Care Act, your private health insurance is legally required to cover addiction treatment on equal terms with any other medical condition.

Understanding how your insurance actually works—your deductible, co-insurance, and out-of-pocket maximum—transforms abstract anxiety into concrete, manageable costs. For most Oregonians with private insurance, comprehensive residential addiction treatment costs far less than anticipated, typically capping out at $3,000-$5,000 through out-of-pocket maximums, regardless of the actual cost of care.

The Verification of Benefits process eliminates uncertainty entirely, providing complete financial transparency before you make any commitment to treatment. Facilities like Pacific Ridge remove the guesswork by working directly with your insurance company, handling prior authorization requirements, and providing clear written cost estimates upfront.

When you compare the out-of-pocket cost of treatment to the devastating financial toll of untreated addiction—emergency room visits, legal fees, lost employment, and chronic health conditions—the choice becomes clear. Treatment isn’t an expense; it’s a high-return investment in your health, your future, and your family’s well-being.

Delaying treatment due to cost fears only prolongs suffering and increases the financial burden over time. Your insurance is designed specifically to help you access the care you need—and it’s there to be used.

Ready to Verify Your Insurance Benefits?

Contact Pacific Ridge today for a free, confidential benefits check. Our admissions specialists will walk you through your coverage, answer all your questions, and provide a clear picture of your out-of-pocket costs—with no obligation and no surprises.

Your recovery is worth fighting for, and it’s more affordable than you think.

References:

- Substance Abuse and Mental Health Services Administration (SAMHSA). (2022). National Survey on Drug Use and Health (NSDUH): State-Level Estimates. https://www.samhsa.gov/data/report/2022-nsduh-state-prevalence-estimates

- Substance Abuse and Mental Health Services Administration (SAMHSA). (2023). Key Substance Use and Mental Health Indicators in the United States. https://www.samhsa.gov/data/report/2022-nsduh-annual-national-report

- Centers for Medicare & Medicaid Services (CMS). (2023). The Mental Health Parity and Addiction Equity Act (MHPAEA). https://www.cms.gov/CCIIO/Programs-and-Initiatives/Other-Insurance-Protections/mhpaea_factsheet

- Kaiser Family Foundation (KFF). (2022). Mental Health and Substance Use Parity: A Primer. https://www.kff.org/mental-health/issue-brief/mental-health-and-substance-use-parity-a-primer/

- Oregon Health Authority (OHA). (2023). Substance Use Disorder Services and Health Coverage. https://www.oregon.gov/oha/HSD/AMH/Pages/SUD.aspx

- American Medical Association (AMA). (2023). Prior Authorization Practice Resources: Overcoming Barriers in Behavioral Health. https://www.ama-assn.org/practice-management/prior-authorization/prior-authorization-practice-resources

- National Institute on Drug Abuse (NIDA). (2020). Principles of Drug Addiction Treatment: A Research-Based Guide (Third Edition) – Is drug addiction treatment worth its cost? https://nida.nih.gov/publications/principles-drug-addiction-treatment-research-based-guide-third-edition

Posted in Treatment

Are you looking for help?

Pacific Ridge is a residential drug and alcohol treatment facility about an hour from Portland, Oregon, on the outskirts of Salem. We’re here to help individuals and families begin the road to recovery from addiction. Our clients receive quality care without paying the high price of a hospital. Most of our clients come from Oregon and Washington, with many coming from other states as well.

Pacific Ridge is a private alcohol and drug rehab. To be a part of our treatment program, the client must voluntarily agree to cooperate with treatment. Most intakes can be scheduled within 24-48 hours.

Pacific Ridge is a State-licensed detox and residential treatment program for both alcohol and drugs. We provide individualized treatment options, work closely with managed care organizations, and maintain contracts with most insurance companies.

Quick links

Recent Posts

Contact Us

Pacific Ridge- 1587 Pacific Ridge Ln SE

Jefferson, OR 97352 - Email:

[email protected] - Phone:

503-506-0101 - Fax:

503-581-8292

- Copyright © 2026 Pacific Ridge - All Rights Reserved. Web Design & SEO by Lithium

- Follow us on